4 Magnitude tabular data

4.1 Introduction

Statistical magnitude tables display sums of observations of a quantitative variable where each sum relates to a group of observations defined by categorical variables observed for a set of respondents.

Respondents are typically companies but can also be individuals or households, etc. Grouping variables typically give information on geography or economic activity or size, etc. of the respondents. The “cells” of a table are defined by cross-combinations of the grouping variables.

Each “table cell” presents a sum of a quantitative variable such as income, turnover, expenditure, sales, number of employees, number of animals owned by farms, etc. These sums are the “cell values” (sometimes also referred to as “cell totals”) of a magnitude table. The individual observations of the variable (for each individual respondent) are the “contributions” to the cell value.

| Industry A | Industry B | … | Total | |

| Region 1 | 540 (12) | 231 (15) | … | |

| Region 2 | 48 (2) | 125 (8) | … | |

| … | … | … | … | |

| Total |

The “dimension” of a table is given by the number of grouping variables used to specify the table. We say that a table contains “margins” or “marginal cells”, if not all cells of a table are specified by the same number of grouping variables. The smaller the number of grouping variables, the higher the “level” of a marginal cell. A two-dimensional table of some business survey may for instance provide sums of observations grouped by economic activity and company size classes. At the same time it may also display the sums of observations grouped by only economic activity or by only size classes. These are then margins/marginal cells of this table. If a sum across all observations is provided, we refer to it as the “total” or “overall total”.

At first sight, one might find it difficult to understand how the kind of summary information published in magnitude tables presents a disclosure risk at all. However, it often occurs that cells of a table relate to a single or to only a few respondents. The number of this kind of small cells in a table will increase, the more grouping variables are used to specify the table, the higher the amount of detail provided by the grouping variables, and the more uneven the distributions of respondents over the categories of the grouping variables.

If a table cell relates to a small group of respondents (or even only one), then publication of the cell value may imply a disclosure risk. This is the case if these respondents could be identified by an intruder using information displayed in the table.

Example 1 Let a table cell display the turnover of companies in the mining sector for a particular region X. Let us assume that company A is the only mining company in this region. This is a fact that will be known to certain intruders (think, for instance, of another mining company B in a neighbouring region Y). So, if that table cell is published, company B would be able to disclose the turnover of company A.

In order to establish if a disclosure risk is connected to the publication of a cell value in a table, and in order to protect against this risk, data providers (like, e.g. National Statistical Institutes) should apply tabular data protection methods. In many countries this is a legal obligation to official statistical agencies. It may also be regarded as a necessary requirement in order to maintain the trust of respondents: After all, if in the instance above company A realizes that company B might, by looking into the published table, disclose the value of turnover it has reported, and if it considers this value as confidential information, it may refuse to respond to that survey in the next period, or (if the survey is compulsory) it may choose to provide incorrect or inaccurate information.

Especially for business statistics, the most popular method for tabular data protection is cell suppression . In tables protected by cell suppression, all values of cells for which a disclosure risk has been established are eliminated from the publication. Alternatively, other methods based on cell perturbation etc. may also be used to protect tabular data. While we focus in this chapter on cell suppression, we will also mention alternatives.

Section 4.2 introduces into the methodological concepts of tabular data protection. In Section 4.2.1 we present the most common methods for disclosure risk assessment for each individual cell of a table (and for special combinations of individual cells). These methods are called “primary” disclosure control methods. Table cells for which a disclosure risk has been established are called “sensitive”, “confidential”, or “unsafe” cells. Primary disclosure risk is usually assessed by applying certain sensitivity rules. Section 4.2.1 explains the concept of sensitivity rules and the most common rules.

While detailed tabulated summary information also on smaller groups of statistical objects (companies by subgroups of subsectors at the district level, households by size and income at the neighbourhood level, etc.) might be of interest to certain user groups, it is also a responsibility (maybe the most important one) of official statistics to provide summary information at a high aggregate level by producing summary statistics on large groups of a population (e.g. for all companies of an economy sector). Because of this, it is not enough to have methodologies to protect individual cells. It implies a need for the so-called “secondary” tabular data protection methodologies.

Assume that a table displays the sum of a variable “Production” by three subsectors of an economy sector. Assume that this sum is sensitive for one of the subsectors and that the table is protected by cell suppression, meaning that the confidential cell value is suppressed.

Example 1a Production (in mill. Euro)

| Sector | Subsector I | Subsector II | Subsector III |

| 56,600 | suppressed (sensitive) |

47,600 (non-sensitive) |

8,002 (non-sensitive) |

With respect to the total production for this sector we distinguish two cases: Either it is foreseen to be published – we then consider it as a cell of the table (e.g. the “total”). If the cell values of the two non-sensitive subsectors and the “total” are displayed, then users of the publication can disclose the cell value for the sensitive subsector by taking the difference between the “total” and the subsector values for the two non-sensitive sectors (56,600 – 47,600 – 8,002 = 998). In order to avoid this, a secondary protection measure for this table has to be taken, e.g. selecting one of the two non-sensitive subsector cells and suppressing it as well. This would be called a “secondary suppression”.

The other option is that the “total” is not foreseen to be displayed / published. Then no secondary protection measure would be needed. In this instance, because the production for one subsector is suppressed, interested users of the table cannot compute the production for the sector on their own – and so the sector-level information is completely lost!

From a general perspective, the purpose of secondary tabular data protection methodologies is chiefly to avoid undesirable effects such as this, ensuring that – while some “small”, primary confidential cells within detailed tables may have to be protected (by cell suppression or by some perturbative method) – sums for larger groups, i.e. the margins of those detailed tables, are preserved to some extent. For cell suppression this means that suppression of marginal cells should be avoided as far as possible. For perturbative methods it means that high level margins should try to be preserved exactly (more or less).

Considering this as the basic idea of secondary protection, after Section 4.2.1 we assume for the remainder of the chapter margins and overall totals always to be part of a table.

In Section 4.2.2 we introduce the concepts of secondary tabular data protection methodologies. The focus will be on cell suppression, but we will also mention other methodologies.

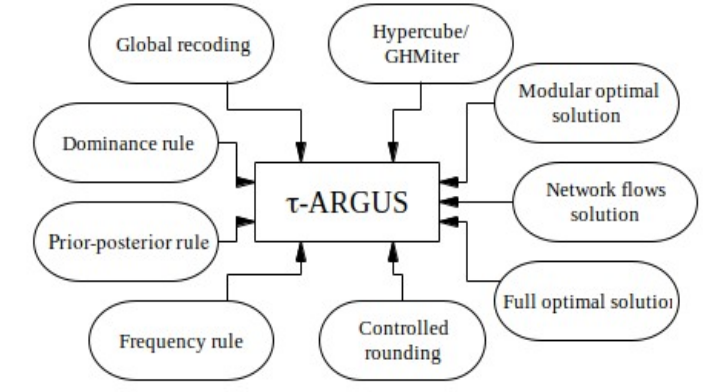

The software package \(\tau\)‑ARGUS (see e.g. Hundepool et al., 2014) provides software tools for disclosure protection methods for tabular data. The latest version of \(\tau\)-ARGUS can be found on GitHub (https://github.com/sdcTools/tauargus/releases). Section 4.3 is concerned with the practical implementation of secondary cell suppression as offered by \(\tau\)‑ARGUS. In Section 4.3.1 we discuss information loss concepts as well as table structures considered by \(\tau\)‑ARGUS. We compare the performance of different algorithms for secondary cell suppression in Section 4.3.2 and give software recommendations. In Section 4.3.3 we explain how to set up procedures for tabular data protection in a practical way and give an introductive example in Section 4.3.4. In Section 4.4 we briefly introduce the methodological concepts of the secondary cell suppression algorithms provided by \(\tau\)-ARGUS. The chapter ends with Section 4.5, introducing Controlled Tabular Adjustment as new emerging protection technique for magnitude tables which could become an alternative to the well-established cell suppression methodologies.

4.2 Disclosure Control Concepts for Magnitude Tabular Data

In this section we explain the main concepts for assessment and control of disclosure risk for magnitude tables.

Section 4.2.1 is concerned with disclosure risk for each individual cell of tables presenting summaries of quantitative variables and will introduce the most common methods used to assess this risk.

In order to preserve the margins of tables to some extent while protecting individual sensitive cells, special disclosure control methodologies have been developed. Section 4.2.2 presents basic concepts of these methodologies, focusing on secondary cell suppression as the most prominent instance. We finish section methods with a brief, comparative overview of alternative methods for tabular data protection.

4.2.1 Sensitive Cells in Magnitude Tables

We begin this section by describing intruder scenarios typically considered by statistical agencies in the context of disclosure control for magnitude tables. Considering these intruder scenarios statistical agencies have developed some ‘safety rules’ as measures to assess disclosure risks. This section will also introduce the most popular rules using some illustrative examples. Finally, we compare rules and give guidance on making a decision between alternative rules.

Intruder scenarios

If a table cell relates to a small group (or even only one) respondent, then publication of the cell value may imply a disclosure risk. This is the case, if these respondents could be identified by an intruder using information displayed in the table. In example 1 of Section 4.1, for the intruder (company B) it is enough to know that the cell value reports the turnover of mining companies in region X. In that example company B is assumed to be able to identify company A as the only mining company in region X. Hence, publication of the cell value implies a disclosure risk: if company B looks into the publication they will be able to disclose the turnover of company A.

But what if a cell value does not relate to one, but to two respondents?

Example 1b Let us assume this time that both companies (A and B) are located in region X, and are the only mining companies there. Let us further assume that they both are aware of this fact. Then again publication of the cell value implies a disclosure risk (this time to both companies): if any of the two companies look into the publication and subtract their own contribution to the cell value (i.e. the turnover they reported) from the cell value, they will be able to disclose the turnover of the other company.

Example 1c Assume now that the table cell relates to more than two respondents. Imagine this time that four companies (A, B, C and D) are located in region X. Then theoretically three of them (B, C and D, say) could form a coalition to disclose the turnover of company A. Such a coalition might be a rather theoretical construct. An equivalent but perhaps more likely scenario could be that of another party who knows the contributions of companies B, C and D (perhaps a financial advisor working for all three companies) who would then be able to disclose also the turnover of company A by subtracting the contributions of B, C and D from the cell value.

The examples above are based on the intruder scenario typical for business data: it is usually assumed, that the “intruders”, those who might be interested in disclosing individual respondent data, may be “other players in the field”, e.g. competitors of the respondent or other parties who are generally well informed on the situation in the part of the economy to which the particular cell relates. Such intruder scenarios make sense, because, unlike microdata files for researchers, tabular data released by official statistics are accessible to everybody – which means they are accessible in particular to those well informed parties.

In the scenarios of example 1 there is a risk that magnitude information is disclosed exactly. But how about approximate disclosure?

Example 1d Let us reconsider the example once more. Assume this time that in region X there are 51 companies that belong to the mining sector, e.g. company A and 50 very small companies S1 to S50. Assume further that 99 % of the turnover in mining in region X is contributed by company A. In that scenario, the cell value (turnover in the mining sector for region X) is a pretty close approximation of the turnover of company A. And even though the potential intruder (in our example mining company B of the neighbour region Y) may not be able to identify all 51 mining companies of region X, it is very likely that they will know that there is one very big company in region X and which company that is.

Sensitivity of variables

The presumption of the sensitivity of a variable often matters in the choice of a particular protection method. For example, especially in the case of tables presenting business magnitude information many agencies decide that this kind of information must be protected also against the kind of approximate disclosure illustrated by example 1d above, because it is so sensitive.

Considering the above explained intruder scenarios statistical agencies have developed some ‘safety rules’ (also referred to as ‘sensitivity rules’ or ‘sensitivity measures’), measures to assess disclosure risks. We will now introduce the most popular rules, starting with an overview presenting formal representation of these rules in Table 4.2. After that, the rules (or rather, classes of rules) will be discussed in detail. We explain in which situations it may make sense to use those rules, using simple examples for illustration where necessary.

Sensitivity rules

Table 4.2 briefly presents the most common sensitivity rules. Throughout this chapter we denote \(x_{1} \geq x_{2} \geq \cdots \geq x_{N}\) the ordered contributions by respondents \(1,2,\ldots,N\), respectively, to a cell with cell total (or cell value) \(X = \sum_{i=1}^N x_{i}\)

| Rule | Definition |

| A cell is considered unsafe, when … | |

| Minimum frequency rule | the cell frequency is less than a pre-specified minimum frequency \(n\) (the common choice is \(n=3\)). |

| \((n,k)\)-dominance rule | the sum of the \(n\) largest contributions exceeds \(k\%\) of the cell total, i.e. \[x_{1} + \ldots + x_{n} > \frac{k}{100} X \tag{4.1}\] |

| \(p\%\)-rule | the cell total minus the 2 largest contributions \(x_{1}\) and \(x_{2}\) is less than \(p\%\) of the largest contribution, i.e.1 \[X - x_{2} - x_{1} < \frac{p}{100}x_{1} \tag{4.2}\] |

1 \(X − x_{n} − \cdots − x_{2} − x_{1} < \frac{p}{100} x_{1}\) for the case of coalitions of \(n-1\) respondents, where \(n>2\)

Note that both the dominance rule and the \(p\%\)-rule are meaningful only when all contributions are non-negative. Moreover, the dominance rule does not make sense for \(k=100\) and neither does the \(p\%\)-rule for \(p = 0\). Both rules are asymptotically equal to minimum frequency rules for \(k\rightarrow 100\), or \(p \rightarrow 0\) respectively.

Both, the dominance rule and the \(p\%\)-rule belong to a class of rules which are referred to as “concentration rules” below.

When cell suppression is used to protect the table, any aggregate (or: cell in a table) that is indeed ‘unsafe’, or ‘sensitive’ according to the sensitivity rule employed, is subject to what is called ‘primary suppression’.

Choice of a particular sensitivity rule is usually based on certain intruder scenarios involving assumptions about additional knowledge available in public or to particular users of the data, and on some (intuitive) notion on the sensitivity of the variable involved.

Minimum frequency rule

When the disseminating agency thinks it is enough to prevent exact disclosure, all cells with at least as many respondents as a certain, fixed minimum frequency \(n\) are considered safe. Example 1 of Section 4.1 (cell value referring to one company in the mining sector of a region) illustrates the disclosure risk for cells with frequency 1. Example 1b above (on two mining companies) shows that there is a similar risk for cells with frequency 2.

Normally the minimum frequency \(n\) will be set to 3.

An exception is the case when for some \(n_0\) larger than 3 the agency thinks it is realistic to assume that a coalition of \(n_0 - 2\) respondents contributing to the same cell may pool their data to disclose the contribution of another respondent. In such a case we set \(n\) to \(n_0\). Example 1c above provides an instance for this case with \(n_0=5\). (The intruder knows the pooled data of \(5 - 2 = 3\) companies (e.g. B, C and D)).

It should be stressed here that a minimum frequency larger than 3 normally does not make much sense, even though in example 1c, for some cells of a table it may happen that such a ‘pooled data’ situation actually occurs. Usually there is no way for an agency to know for which cell which size to assume for the ‘pool’. Let us assume, for instance, that in a cell with 100 respondents 99 are in the stock market and are therefore obliged to publish data which are also their contributions to that cell value. Then we should consider 99 as the size of the pool, because anybody could add up (i.e. pool) these 99 published data values in order to disclose the (confidential) contribution of company 100 who is not in the stock market. But should the agency really consider all cells with less than 101 respondents as unsafe?

Concentration rules

A published cell total is of course always an upper bound for each individual contribution to that cell. This bound is the closer to an individual contribution, the larger the size of the contribution. This fact is the mathematical foundation of the well-known concentration rules. Concentration rules like the dominance and \(p\%\)‑rule make sense only if it is assumed specifically that the intruders are able to identify the largest contributors to a cell. The commonly applied sensitivity rules differ in the particular kind and precision of additional knowledge assumed to be around.

When a particular variable is deemed strongly confidential, preventing only exact disclosure may be judged inadequate. In such a case a concentration rule should be specified. For reasons that will be explained below, we recommend use of the so called \(p\%\) ‑rule. Another, well known concentration rule is the ‘\(n\) respondent, \(k\) percent’ dominance rule. Note, that it is absolutely essential to keep the parameters of a concentration rule confidential!

Traditionally, some agencies use a combination of a minimum frequency rule together with a \((1,k)\)‑dominance rule. This approach, however, is inadequate, because it ignores the problem that in some cases the contributor with the second largest contribution to a cell which is non-sensitive according to this rule is able to derive a close upper estimate for the contribution of the largest one by subtracting her own contribution from the aggregate total. Example 1 provides an instance.

Example 1 Application of the (1,90)-rule. Let the total value of a table cell be \(X = 100,000\), let the two largest contributions be \(x_{1} = 50,000\) and \(x_{2} = 49,\!000\). Since \(50,\!000 < \frac{90}{100} 100,\!000\) the cell is safe according to the \((1,90)\)-rule: there seems to be no risk of disclosure. But the second largest contributor is able to derive an upper estimate \({\hat{x}}_{1} = 100,\!000 − 49,\!000 = 51,\!000\) for the largest contribution which overestimates the true value of \(50,000\) by \(2\%\) only: quite a good estimate!

Unlike the \((1,k)\)-dominance rule, both the \((2,k)\)‑dominance rule and \(p\%\)‑rule take the additional knowledge of the second largest contributor into account properly. Of the two, the \(p\%\)‑rule should be preferred, because the \((2,k)\)-dominance rule has a certain tendency for overprotection, as we will see in the following.

\(p\%\)-rule and dominance-rule

We will show in the following that, according to both types of concentration rules, an aggregate total (i.e. cell value) \(X\) is considered as sensitive, if it provides an upper estimate for one of the individual contributions that is relatively close to this contribution.

Assume that there are no coalitions of respondents, i.e. there are no intruders knowing more than one of the contributions. Then the closest upper estimate of any other contribution can be obtained by the second largest contributor, when it subtracts its own contribution \(x_{2}\) from the aggregate total (i.e. cell value) \(X\) to estimate the largest contribution (\({\hat{x}}_{1} = X - x_{2}\)) as seen in example 1. All other scenarios of a contributor subtracting its own value from the total, to estimate another, result in larger relative error. In the, rather unlikely, scenario that \(n - 1\) (for \(n > 2\)), respondents pool their data in order to disclose the contribution of another, the closest upper estimate of any other contribution can be obtained by the coalition of respondents \(2, 3,\ldots, n\) when they estimate \({\hat{x}}_{1} = X - x_{2} - x_{3} - \ldots - x_{n}\).

The question is now, how to determine whether such an estimate is ‘relatively close’.

Application of the \(p\%\)-rule yields that the upper estimate \({\hat{x}}_{1}\) will overestimate the true value by at least \(p\%\) for any non-sensitive cell, i.e. \({\hat{x}}_{1} - x_{1} \geq \frac{p}{100} x_{1}\) . That is, the \(p\%\)‑rule sets the difference between estimate and true value of the largest contribution in relation to the value of the largest contribution itself.

When we adapt relation (4.1) in table 1 (see definition of the \((n,k)\)-rule) to the case of \(n = 2\), subtract both sides from \(X\) and then divide by \(X\) the result is \[ (X - x_{2}) - x_{1} < \frac{100 - k}{100} X \tag{4.3}\]

In this formulation, the \((2,k)\)-rule looks very similar to the formulation of the \(p\%\)-rule given by (4.2). Both rules define an aggregate to be sensitive, when the estimate \(\hat{x}_{1} = X - x_{2}\) does not overestimate the true value of \(x_{1}\) ‘sufficiently’. The difference between both rules is in how they determine this ‘sufficiency’. According to the \(p\%\)-rule, it is expressed as a rate (i.e. \(p\%\)) of the true value of the largest contribution \(x_{1}\), while according to the \((2,k)\)‑rule, it is expressed as a rate (i.e. \((100-k)\%\)) of the aggregate total \(X\). Considering this, the concept of the \(p\%\)-rule seems to be more natural than that of the \((2,k)\)-rule.

\((2,k)\)-rules correspond to \(p\%\)-rules in the following way:

If \(k\) is set to \(100 \frac{100}{100+p}\) then

any aggregate, which is safe according to the \((2,k)\)‑rule, is also safe according to the \(p\%\)-rule (this will be proven below), but

not any aggregate, which is safe according to the \(p\%\)-rule, is also safe according to this \((2,k)\)-rule. An example is given below (example 2). In these cases the aggregate could be published according to the \(p\%\)-rule, but would have to be suppressed according to the \((2,k)\)-rule.

Based on the above explained idea, that the concept of the \(p\%\)-rule is more natural than that of the \((2,k)\)-rule, we interpret this as a tendency for over-protection in the \((2,k)\)-rule. Example 2 below is an instance for this kind of over-protection.

We therefore recommend use of the \(p\%\)‑rule instead of a \((2,k)\)‑dominance rule.

How to obtain the \(p\) parameter?

When we replace a \((2,k)\)‑dominance rule, by a \(p\%\)‑rule, the natural choice is to derive the parameter \(p\) from \(k = 100 \frac{100}{100 + p}\) , e.g. to set \(p = 100 \frac{100 - k}{k}\)

Thus, a \((2,80)\)‑dominance rule would be replaced by a \(p\%\)‑rule with \(p = 25\), a \((2,95)\)‑dominance rule by a \(p\%\)‑rule with \(p = 5.26\) .

If we also derive \(p\) from this formula, when replacing a \((1,k)\)‑dominance rule, we will obtain a much larger number of sensitive cells. In addition to the cells which are unsafe according to the \((1,k)\)-dominance rule which will then also be unsafe according to the \(p\%\)‑rule, there will be cells which were safe according to the \((1,k)\)‑dominance rule, but are not safe according to the \(p\%\)‑rule, because the rule correctly considers the insider knowledge of a large second largest contributor. We could then put up with this increase in the number of sensitive cells. Alternatively, we could consider the number of sensitive cells that we used to assign (with the \((1,k)\)-dominance rule) as a kind of a maximum-price we are prepared to ‘pay’ for data protection. In that case we will reduce the parameter \(p\). The effect will be that some of the cells we used to consider as sensitive according to the \((1,k)\)-dominance rule will now not be sensitive. But this would be justified because those cells are less sensitive as the cells which are unsafe according to the \(p\%\)-rule, but are not according to the former \((1,k)\)-dominance rule, as illustrated above by Example 1.

Example 2 Let \(p = 10\), then \(k = 100 \frac{100}{100 + p} = 90.9\), let the total value of a table cell be \(X = 110,\!000\), let the largest two contributions be \(x_{1} = 52,\!000\), and \(x_{2} = 50,\!000\).

Then \[ \hat{x_1} = X - x_{2} = 110,\!000 − 50,\!000 = 60,\!000 \] and \[ 100 \frac{\hat{x_1} - x_1}{x_1}=100 \frac{60,\!000 - 52,\!000}{52,\!000}=15.4 \] i.e. the upper estimate \(\hat{x_1} = X - x_{2}\) will overestimate the true value by \(15.4\%\). So the aggregate is safe according to the \(p\%\)-rule at \(p = 10\).

On the other hand the two largest contributions are \(x_{1} + x_{2} = 102,\!000\). As \(102,000 > \frac{100} {100 + p } X = 100,\!000\) the aggregate is not safe according to the \((2,k)\)-rule.

Proof of A.

For an aggregate which is safe according to the \((2,k)\)‑rule with \(k = 100 \cdot \frac{100}{100 + p}\) the following will hold: \[

x_{1} \leq \frac{k}{100} \cdot X = \frac{100}{100 + p} X

\tag{4.4}\] and \[\frac{ \left( X - x_{2} \right) - x_{1} }{ X } \geq 1 - \frac{k}{100} = 1 - \frac{100}{100 + p} = \frac{p} {100 + p}

\tag{4.5}\] (c.f. (4.3) ).

This is equivalent to \[

\frac{ \left( X - x_{2} \right) - x_{1} }{ x_1 } \geq \frac{p}{100+p}\frac{X}{x1}

\tag{4.6}\] From (4.4) it follows that \[

\frac{ p }{ 100 + p } \frac{ X }{ x_{1} } \geq \frac{p}{100}

\] And hence from (4.6) that \[\frac{ \left( X - x_{2} \right) - x_{1} } { x_{1} } \geq \frac{p}{ 100 + p } \cdot \frac{ X }{ x_{ 1 } } \geq \frac{ p }{ 100 }

\]

The \((p,q)\)-rule

A well known extension of the \(p\%\)-rule is the so called prior‑posterior \((p,q)\)‑rule. With the extended rule, one can formally account for general knowledge about individual contributions assumed to be around prior to the publication, in particular that the second largest contributor can estimate the smaller contributions \(X_{R} = \sum_{ i > 2 } x_{i}\) to within \(q\%\). An aggregate is then considered unsafe when the second largest respondent could estimate the largest contribution \(x_{1}\) to within \(p\) percent of \(x_{1}\) , by subtracting her own contribution and this estimate \({\hat{X}}_{R}\) from the cell total, i.e. when \(|\left( X - x_{2} \right) - x_{1} - {\hat{X}}_{R}| < \frac{p}{100} x_{1}\). Because \(\left( X - x_{2} \right) - x_{1} = X_{R}\), the left hand side is assumed to be less than \(\frac{q}{100} X_{R}\). So the aggregate is considered to be sensitive, if \(X_{R} < \frac{p}{q} x_{1}\). Evidently, it is actually the ratio \(\frac{p}{q}\) which determines which cells are considered safe, or unsafe. Therefore, any \((p,q)\)‑rule with \(q < 100\) can also be expressed as \(( p^*, q^*)\)‑rule, with \(q^* = 100\) and \[

p^* := 100 \frac{p}{q}

\tag{4.7}\]

Of course we can also adapt the \((n,k)\)-dominance rule to account for \(q\%\) relative a priori bounds: Let e.g. \(n = 2\). According to (4.3) above, an aggregate should then be considered unsafe when the second largest respondent could estimate the largest contribution \(x_{1}\) to within \((100 - k)\) percent of \(X\) , by subtracting her own contribution and the estimate \({\hat{X}}_{R}\) from the cell total, i.e. when \(|\left( X - x_{2} \right) - x_{1} - {\hat{X}}_{R}| < (100 - k)/100 X\). Just as in the case of the \(p\%\)-rule, we see that the aggregate is sensitive, when \(X_{R} < \frac{100 - k}{q} X\), and that for given parameters \(k\) and \(q\) the parameter \(k^*\) corresponding to \(q^* = 100\) should be chosen such that \[ \frac{100-k^*}{100} = \frac{100-k}{q} \tag{4.8}\]

For a more analytical discussion of sensitivity rules the interested reader is referred to (Cox, 2001), for more generalized formulations considering coalitions to (Loeve, 2001).

Negative contributions

When disclosure risk has to be assessed for a variable that can take not only positive, but also negative values, we suggest to reduce the value of \(p\) (or increase \(k\), for the dominance-rule, resp.). It may even be adequate to take that reduction even to the extent of replacing a concentration rule by a minimum frequency rule. This recommendation is motivated by the following consideration. Above, we have explained that the \(p\%\)‑rule is equivalent to a \((p,q)\)-rule with \(q=100\). When contributions may take negative, as well as positive values, it makes sense to assume that the bound \(q_{-}\) for the relative deviation of a priori estimates \({\hat{X}}_{R}\) exceeds \(100\%\). This can be expressed as \(q_{-} = 100 f\), with \(f > 1\). According to (4.7) the \(p\) parameter \(p_f\) for the case of negative/positive data should be chosen as \(p_{f} = 100 \frac{p}{q_{-}} = 100 \frac{p}{100 f} = \frac{p}{f} < p\). That means particularly that for large \(f\) the \(p\%\)-rule with corresponding parameter \(p_{f}\) is asymptotically equal to the minimum frequency rule (c.f. the remark just below Table 4.2).

In case of the dominance rule, because of (4.8), \(k_{f}\) can be determined by \(\frac{100 - k_{f}}{100} = \frac{100 - k}{100 f}\), and because \(f > 1\) this means that \(k_{ f } > k\). For large \(f\) the dominance rule with parameter \(k_{ f }\) will be asymptotically equal to the minimum frequency rule.

Waivers

Sometimes, respondents authorize publication of an aggregate even if this publication might cause a risk of disclosure for their contributions. Such authorizations are also referred to as ‘waivers’. When \(s\) is the largest respondent from which no such waiver has been obtained, and \(r\) is the largest respondent except for \(s\) then for any pair \((i,j)\), \(i \neq j\) of respondents, where no waiver has been obtained from \(j\), it holds \(x_{i} + x_{j} \leq x_{r} + x_{s}\). Therefore, we will be able to deal with such a situation properly, if we reformulate the concentration rules as

\(X - x_{s} - x_{r} < \frac{p}{100} x_{s},\) for the \(p\%\)-rule,

and

\(x_{r} + x_{s} > \frac{k}{100} X,\) for the \((2,k)\)-dominance rule.

Foreign trade rules

In foreign trade statistics traditionally a special rule is applied. Only for those enterprises that have actively asked for protection of their information special sensitivity rules are applied. This implies that if the largest contributor to a cell asks for protection and contributes over a certain percentage to the cell total, that cell is considered a primarily unsafe cell.

Given the normal level of detail in the foreign trade tables the application of the standard sensitivity rules would imply that a very large proportion of the table should have been suppressed. This is considered not to be a desirable situation and for a long time there have not been serious complaints. This has led to this special rule. And this rule has a legal basis in the European regulation 638/2004 https://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=CELEX:32004R0638:EN:HTML.

In \(\tau\)‑ARGUS special options (the request rule) have been introduced to apply this rule. The secondary cell suppression will be done in the standard way.

Holdings

In many datasets, especially economic datasets, the reporting unit is different from the entities we want to protect. Often companies have several branches in various regions. So the marginal cell may have several contributions but from one company only. Therefore it might be a mistake to think that such a cell is safe if we look only at the largest two contributors, while the largest three might belong to only one company.

We need to group the contributions from one company together to one contribution before we can apply the sensitivity rules.

There is no problem in making the cell totals because we are only interested in the sum of the contributions.

In \(\tau\)‑ARGUS it is possible to take this into account by using the holding option.

Sampling weights

Often tables are created from datasets based on sample surveys and NSIs collect a lot of their information this way. There are two reasons why disclosure risk assessment may also be necessary for a sample survey: especially in business surveys the common approach is to sample with unequal probabilities. The first is that large companies are often sampled with probability 1. Typically it will be the case for some of the aggregates foreseen for a publication that all respondents have been sampled with probability 1. In the absence of non-response, for such an aggregate, the survey data are data for the full population. Secondly even, if sampling probabilities are smaller than 1, if an aggregate relates to a strongly skewed population, and the sampling error is small, then the probability is high that the survey estimate for the aggregate total may also be a close estimate for the largest unit in that population. It makes sense therefore to assess the disclosure risk for survey sample estimates, if the sampling errors are small but the variables are strongly sensitive. The question is then, how to determine technically, if a sample survey aggregate should be considered safe, or unsafe. The following procedure is used in \(\tau\)‑ARGUS:

For sample survey data each record has a sampling weight associated with it. These sampling weights are constructed such that the tables produced from this datasets will resemble as much as possible the population, as if the table had been based on a full census.

Making a table one has to take into account these sampling weights. If the data file has a sampling weight, specified in the metadata, the table can be computed taking these weights into account. For making a cell total this is a straightforward procedure, however the sensitivity rules have to be adapted to the situation where we do not know the units of the population with the largest values.

One option is the following approximation:

Example A cell with two contributions:

100, weight 4

10, weight 7

The weighted cell value then equals (4 \(\times\) 100) + (7 \(\times\) 10) = 470. Without considering the weights there are only two contributors to the cell: one contributing 100 and another contributing 10. However by taking account of the sampling weights the individual contributions can be approximated as 100, 100, 100, 100, 10, 10, 10, 10, 10, 10 and 10. The largest two contributors are now 100 and 100. These are regarded as the largest two values for application of the safety rules. If the weights are not integers, a simple extension is applied.

Note:

This procedure cannot be applied in combination with the holding concept, because naturally for the approximate contributions it is unknown which holding they belong to.

It should also be noted here that with the above procedure it may happen that a cell is considered safe, even though the sample estimate of the cell total provides a very close estimate of the unit in the population with the largest value. Assume e.g. the sequence of values in the full population to be 900, 100, 100, and seven times 5. Then the population total would be 1135. Assume that we sampled two units, both with a value of 100, but with different probabilities so that the sampling weights for the two are 1, and 9, respectively, yielding a population estimate of 1000 which will not be sensitive according to the above procedure. If the second largest unit as an intruder subtracts her own contribution (= 100) from the population estimate she will obtain an estimate of the value of the largest unit which exactly matches the true value of 900. But there is of course a sampling error connected to this estimate and this fact should be considered by the intruder.

On the other hand, there is a certain tendency for overprotection associated to the above procedure, i.e. there is a chance that according to the above procedure an aggregate is unsafe, when in fact it is not. Assume e.g. the sequence of values in the full population to be 100, 50, 50, 1, 1. Assume we have sampled (with unequal probabilities) the unit with value 100 with a sampling weight of 2 associated to it, and one of the units with value 1 with a sampling weight of 3. According to the above procedure two values of 100 would be considered as largest contribution for an estimated cell total of 203 which according to for instance a \(p\%\)-rule would be considered as sensitive for any \(p>3\) . But in fact, even the second largest unit in the population with a value of 50 will overestimate the value 100 of the largest unit by about 50% when it subtracts her own contribution from the population estimate of 203.

This tendency for overprotection can be avoided, when, instead of the above procedure, in the case of sample surveys we replace for instance for the \(p\%\)‑rule the formulation (4.2) of Table 4.2 by the following \[ \hat{X} - x_{2}^{s} - x_{1}^{s} < \frac{p}{100} x_{1}^{s} \tag{4.9}\] where \(\hat{X}\) denote the estimated population total, and \(x_{i}^{s}\), \(i = 1,2\), the largest two observations from the sample.

The difference between this, and the above procedure is that with (4.9) we consider as intruder the respondent with the second largest contribution observed in the sample, whereas according to the above procedure, whenever the sampling weight of the largest respondent is 2 or more, an ‘artificial’ intruder is assumed who contributes as much as the largest observation from the sample.

Considering formulation (4.3) of the dominance-rule, it is straightforward to see that we can adapt (4.9) to the case of dominance‑rules by \[ x_{1}^{s} + \ldots + x_{n}^{s} > \frac{k}{100} \hat{X} \tag{4.10}\]

It is also important to note in this context that sampling weight should be kept confidential, because otherwise we must replace (4.9) by \[ \hat{X} - w_{2} x_{2}^{s} - w_{1} x_{1}^{s} < \frac{p}{100} x_{1}^{s} \tag{4.11}\]

where \(w_{i}\), \(i=1,2\), denote the sampling weights. Obviously, according to (4.11) more aggregates will be sensitive.

Considering this as the basic idea of secondary protection, after Section 4.2.1 we assume for the remainder of the chapter margins and overall totals always to be part of a table.

In Section 4.2.2 we introduce into the concepts of secondary tabular data protection methodologies.

4.2.2 Secondary tabular data protection methods

For reasons explained in the introduction of this chapter, we assume here that tables always include margins and overall totals along with their ‘inner’ cells. Thus, there is always a linear relationship between cells of a table. (Consider for instance example 1a of the introduction to this chapter: The sector result (say: \(X_T\)) is the sum of the three sub-sector results (\(X_1\) to \(X_3\)), i.e. the linear relationship between these four cells is given by the relation \(X_T = X_1 + X_2 + X_3\). As we have seen in example 1a, if it has been established that a disclosure risk is connected to the release of certain cells of a table, then it is not enough to prevent publication of these cells. Other cells must be suppressed (so called ‘complementary’ or ‘secondary’ suppressions), or be otherwise manipulated in order to prevent the value of the protected sensitive cell being recalculated through f.i. differencing.

Within this section we explain the methodological background of secondary tabular data protection methods.

At the end of the section we give a brief comparison of secondary cell suppression, partial suppression and controlled tabular adjustment as alternative disclosure limitation techniques.

When a table is protected by cell suppression, by making use of the linear relation between published and suppressed cell values in a table with suppressed entries, it is always possible for any particular suppressed cell of a table to derive upper and lower bounds for its true value. This holds for either tables with non-negative values, and those tables containing negative values as well, when it is assumed that instead of zero, some other (possibly tight) lower bound for any cell is available to data users in advance of publication. The interval given by these bounds is called the ‘feasibility interval’.

Example 3 This example (Geurts, 1992, Table 10, p 20) illustrates the computation of the feasibility interval in the case of a simple two-dimensional table where all cells may only assume non-negative values:

| 1 | 2 | Total | |

|---|---|---|---|

| 1 | \(X_{11}\) | \(X_{12}\) | 7 |

| 2 | \(X_{21}\) | \(X_{22}\) | 3 |

| 3 | 3 | 3 | 6 |

| Total | 9 | 7 | 16 |

For this table the following linear relations hold:

\[\begin{align} X_{11} + X_{12} &= 7 \quad \text{(R1)} \\ X_{21} + X_{22} &= 3 \quad \text{(R2)} \\ X_{11} + X_{21} &= 6 \quad \text{(C1)} \\ X_{12} + X_{22} &= 4 \quad \text{(C2)} \\ \end{align}\]

with \(X_{ij} \geq 0, \forall (i,j)\). Using linear programming methodology, it is possible to derive systematically for any suppressed cell in a table an upper bound \(\left(X^{\max} \right)\) and a lower bound \(\left( X^{\min} \right)\) for the set of feasible values. In the example above, for cell (1,1) these bounds are \(\left( X_{11}^{\min} \right)\) = 3 and \(X_{11}^{\max}\) = 6 .

In this simple instance, however, we do not need linear programming technology to derive this result: Because of the first column relation (C1) \(X_{11}\) must be less or equal 6, and because of the second row relation (R2) \(X_{21}\) must be less or equal 3. Therefore, and because of the first column relation (C1) \(X_{11}\) must be at least 3.

A general mathematical statement for the linear programming problem to compute upper and lower bounds for the suppressed entries of a table is given in Fischetti and Salazar (2000).

In principle, a set of suppressions (the ‘suppression pattern’) should only be considered valid, if the bounds for the feasibility interval of any sensitive cell cannot be used to deduce bounds on an individual respondent contribution contributing to that cell that are too close according to the sensitivity rule employed. For a mathematical statement of that condition, we determine safety bounds for primary suppressions. We call the deviation between those safety bounds and the true cell value ‘upper and lower protection levels’. The formulas of Table 4.4 can be used to compute upper protection levels. Out of symmetry considerations the lower protection level is often set identical to the upper protection level.

| Sensitivity rule | Upper protection level |

|---|---|

| \((1,k)\)-rule | \(\frac{100}{k}x_1 - X\) |

| \((n,k)\)-rule | \(\frac{100}{k} \cdot (x_{1} + x_{2} + \cdots + x_{n}) − X\) |

| \(p\%\)-rule | \(\frac{p}{100} \cdot x_{1} − (X − x_{1} − x_{2})\) |

| \((p,q)\)-rule | \(\frac{p}{q} \cdot x_{1} − (X − x_{1} − x_{2})\) |

Note that we recommend using protection levels of zero when instead of a concentration rule only a minimum frequency rule has been used for primary disclosure risk assessment. As explained in 4.2.1, minimum frequency rules (instead of concentration rules) should only be used, if it is enough to prevent exact disclosure only. And in such a case, a protection level of zero should be enough. Using \(\tau\)-ARGUS this can be achieved by setting the parameter ‘minimum frequency range’ to zero.

If the distance between upper bound of the feasibility interval and true value of a sensitive cell is below the upper protection level computed according to the formulas of Table 4.4, then this upper bound could be used to derive an estimate for individual contributions of the sensitive cell that is too close according to the safety rule employed, which can easily be proven along the lines of Cox (1981).

Example 4 Cell \(X = 330\) with 3 contributions of distinct respondents \(x_{1}=300,\ x_{2}=20,\ x_{3}=10\) is confidential (or ‘unsafe’) according to the \((1,85)\)- dominance rule. If the feasible upper bound \(X^{\max}\) for this confidential cell value is less than \(\frac{100}{85} \cdot x_{1} = 352.94\) , then it will provide an upper estimate for the largest contribution \(x_{1}\) which is too close according to the \((1,85)\)-dominance rule.

Example 5 proves the formula given in Table 4.4 for the case of the \(p\%\)-rule:

Example 5 Let \(X + U\) be the upper bound of the feasibility interval for a cell with cell value \(X\) . The second largest respondent can then deduce an upper bound \(x_{1}^{U}\)by subtracting its own contribution from that upper bound: \(x_{1}^{U} = X + U - x_{2}\). According to the definition of the \(p\%\)-rule proper protection means that \(x_{1}^{U} \geq \left( 1 + \frac{p}{100} \right) \cdot x_{1}\). So, if the feasibility interval provides upper protection, it must hold that \(U \geq \left( 1 + \frac{p}{100} \right) \cdot x_{1} - X + x_{2} = p/100 \cdot x_{1} - \left( X - x_{1} - x_{2} \right)\).

The distance between upper bound of the feasibility interval and true value of a sensitive cell must exceed the upper protection level; otherwise the sensitive cell is not properly protected. This safety criterion is a necessary, but not always sufficient criterion for proper protection! It is a sufficient criterion, when the largest respondent makes the same contribution also within the combination of suppressed cells within the same aggregation (a row or column relation of the table, for instance), and when no individual contribution of any respondent (or coalition of respondents) to such a combination of suppressed cells is larger than the second largest respondent’s (or coalition’s) contribution.

Cases where the criterion is not sufficient arise typically, when the only other suppressed cell within the same aggregation is a sensitive cell too (and not the marginal cell of the aggregation), or when the same respondent can contribute to more than one cell within the same aggregation. In these cases, it may turn out that the individual contribution of a respondent may still be disclosed, even though the upper bound of the feasibility interval is well away from the value of the sensitive cell to which this respondent contributes. The most prominent case is that of two cells with only one single contributor (a.k.a. ‘singletons’) within the same aggregation. No matter how large the cell values, because they both know their own contribution of course, both can use this additional knowledge to disclose the other’s contribution. For an analytical discussion of these issues see Cox(2001). In principle, a suppression pattern should not be considered as valid, when certain respondents can use their insider knowledge (on their own contribution to a cell) to disclose individual contributions of other respondents.

The problem of finding an optimum set of suppressions known as the ‘secondary cell suppression problem’ is to find a valid set of secondary suppressions with a minimum loss of information connected to it. For a mathematical statement of the secondary cell suppression problem see e.g. Fischetti and Salazar (2000).

However, cell suppression is not the only option to protect magnitude tables. As one alternative to cell suppression, ‘Partial Suppression’ has been suggested in Salazar (2003). The partial suppression problem is to find a valid suppression pattern, where the size of the feasibility intervals is minimal. The idea of the partial suppression method is to publish the feasibility intervals of the resulting suppression pattern. Because there is a perception that the majority of users of the publications prefer the statistical agencies to provide actual figures rather than intervals, and partial suppression tends to affect more cells than cell suppression, this method has not yet been implemented.

Another alternative method for magnitude table protection is known as ‘Controlled Tabular Adjustment’ (CTA) suggested for instance in Cox and Dandekar (2002), Castro (2003), or Castro and Giessing (2006). CTA methods attempt to find the closest table consistent with the constraints imposed by the set of table equations and by the protection levels for the sensitive cells, of course taking into account also bounds on cell values available to data users in advance of publication, like non-negativity. This adjusted table would then be released instead of the original table.

4.3 The \(\tau\)‑ARGUS Implementation of Cell Suppression

The software package \(\tau\)‑ARGUS provides software tools for disclosure protection methods for tabular data. This can be achieved by modifying the table so that it contains less, or less detailed, information. \(\tau\)‑ARGUS allows for several modifications of a table: a table can be redesigned, meaning that rows and columns can be combined; sensitive cells can be suppressed and additional cells to protect these can be found in some optimal way (secondary cell suppression). Several alternative algorithms for the selection of secondary suppressions are available in \(\tau\)‑ARGUS, e.g. the Hypercube/GHMiter method, a Modular and a Full optimal solution, and a method based on a network flow algorithm. Instead of cell suppression one could also use other methods for disclosure control of tables. One of these alternative methods is Controlled Rounding. However, use of Controlled Rounding is more common for frequency tables.

We start this section by introducing the basic issues related to the question of how to properly set up a tabular data protection problem for a given set of tables that are intended to be published, discussing tabular data structures, and particularly tables with hierarchical structures. Section 4.3.2 provides an evaluation of algorithms for secondary cell suppression offered by \(\tau\)-ARGUS, including a recommendation on which tool to use in which situation. After that, in Section 4.3.3 we give some guidance on processing table protection efficiently, especially in the case of linked tables. We finish the section with an introductive example in Section 4.3.4.

The latest version of \(\tau\)-ARGUS can be found on GitHub (https://github.com/sdcTools/tauargus/releases).

4.3.1 Setting up a Tabular Data Protection Problem in Practice

At the beginning of this section we explain the basic concept of tables in the context of tabular data protection, and complex structures like hierarchical and linked tables. In order to find a good balance between protection of individual response data and provision of information – in other words, to take control of the loss of information that obviously cannot be avoided completely because of the requirements of disclosure control, it is necessary to somehow rate the information loss connected to a cell that is suppressed. We therefore complete this section by explaining the concept of cell costs to rate information loss.

Table specification

For setting up the mathematical formulation of the protection problems connected to the release of tabulations for a certain data set, all the linear relations between the cells of those tabulations have to be considered. This leads us to a crucial question: What is a table anyway? In the absence of confidentiality concerns, a statistician creates a table in order to show certain properties of a data set, or to enhance comparison between different variables. So a single table might literally mix apples and oranges. Secondly, statisticians may wish to present a number of those ‘properties’, publishing multiple tables from a particular data set. Where does one table end and the next start? Is the ideal table one that fits nicely on a standard-size sheet of paper? With respect to tabular data protection, we have to think of tables in a different way:

Magnitude tables display sums of observations of a quantitative variable, the so-called ‘response variable’. The sums are displayed across all observations and/or within groups of observations. These groups can be formed by grouping the respondents according to certain criteria such as their economic activity, region, size class of turnover, legal form, etc. In that case the grouping of observations is defined by categorical variables observed for each individual respondent, the ’explanatory variables’. It also occurs that observations are grouped by categories of the response variable, for instance fruit production into apples, pears, cherries, etc.

The “dimension” of a table is given by the number of grouping variables used to specify the table. “Margins” or “marginal cells” of a table are those cells, which are specified by a smaller number of grouping variables. The smaller the number of grouping variables, the higher the “level” of a marginal cell. A two-dimensional table of some business survey may for instance provide sums of observations grouped by economic activity and company size classes. At the same time it may also display the sums of observations grouped by only economic activity or by only size classes. These are then margins/marginal cells of this table. If a sum across all observations is provided, we refer to it as the “total” or “overall total”.

Note that tables presenting ratios or indexes typically do not define a tabular data protection problem, because there are no additive structures between the cells of such a table, and neither between a cell value, and the values of the contributing units. Think, for instance, of mean wages, where the cell values would be a sum of wages divided by a sum over the number of employees of several companies. However, there may be exceptions: if, for instance, it is realistic to assume that the denominators (say, the number of employees) can be estimated quite closely, both on the company level and on the cell level, then it might indeed be adequate to apply disclosure control methods based, for example, on the enumerator variable (in our instance: the wages).

Hierachical, linked tables

Data collected within government statistical systems must meet the requirements of many users, who differ widely in the particular interest they take in the data. Some may need community-level data, while others need detailed data on a particular branch of the economy but no regional detail. As statisticians, we try to cope with this range of interest in our data by providing the data at several levels of detail. We usually combine explanatory variables in multiple ways, when creating tables for publication. If two tables presenting data on the same response variable share some categories of at least one explanatory variable, there will be cells which are presented in both tables – those tables are said to be linked by the cells they have in common. In order to offer a range of statistical detail, we use elaborate classification schemes to categorize respondents. Thus, a respondent will often belong to various categories of the same classification scheme ‑ for instance a particular community within a particular county within a particular state ‑ and may thus fall into three categories of the regional classification.

The structure between the categories of hierarchical variables also implies sub-structure for the table. When, in the following, we talk about sub-tables without substructure, we mean a table constructed in the following way:

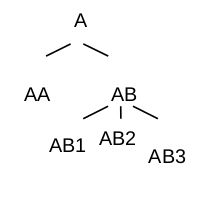

For any explanatory variable we pick one particular non-bottom-level category (the ‘food production sector’ for instance). Then we construct a ‘sub-variable’. This sub-variable consists only of the category picked in the first step and those categories of the level immediately below belonging to this category (bakers, butchers, etc.). After doing that for each explanatory variable the table specified through a set of these sub-variables is free from substructure then, and is a sub-table of the original one. Any cell within the sub-table does also belong to the original table. Many cells of the original table will appear in more than one sub-table: The sub-tables are linked. Example 6 provides a simple instance of a one-dimensional table with hierarchical structure.

Example 6 Assume the categories A, AA, AB, AB1, AB2, and AB3 of some variable EXP resemble a hierarchical structure as depicted in Figure 4.2 below:

Let the full table present turnover by the categories of EXP. Then the two subtables of this table will be:

| EXP | Turnover | |

| A | ||

| AA | ||

| AB |

| EXP | Turnover | |

| AB | ||

| AB1 | ||

| AB2 |

Note that cell AB appears in both subtables

Of course, when using cell suppression methods to protect a set of linked tables, or sub-tables, it is not enough to select secondary suppressions for each table (or sub-table) separately. Otherwise it might for instance happen that the same cell is suppressed in one table because it is used as secondary suppression, while within another table it remains unsuppressed. A user comparing the two tables would then be able to disclose confidential cells in the first table. A common approach is to protect tables separately, but note any complementary suppression belonging also to one of the other tables; suppress it in this table as well, and repeat the cell suppression procedure for this table. This approach is called a ‘backtracking procedure’. Although within a backtracking process for a hierarchical table the cell-suppression procedure will usually be repeated several times for each sub-table, the number of computations required for the process will be much smaller than when the entire table is protected all at once.

It must however be stressed, that a backtracking procedure is not global according to the denotation in Cox (2001). See Cox (2001) for discussion of problems related to non-global methods for secondary cell suppression.

For mathematical formulation of linked tables structures see de Wolf (2007) and de Wolf, Giessing (2008).

Cell costs

The challenge of tabular data protection is to preserve as much information in the table as possible, while creating the required uncertainty about the true values of the sensitive cells, as explained in the previous section. It is necessary to somehow rate the information content of data, in order to be able to express the task of selecting an ‘optimal set’ of secondary suppressions, or, alternatively, of adjusting a table in an optimal way, as mathematical programming problem. Information loss is expressed in these mathematical models as the sum of costs associated to the secondary suppressions, or non-sensitive cells subject to adjustment.

For cell suppression, the idea of equating a minimum loss of information with the smallest number of suppressions is probably the most natural concept. This would be implemented technically by assigning identical costs to each cell. Yet experience has shown that this concept often yields a suppression pattern in which many large cells are suppressed, which is undesirable. In practice other cost functions, based on cell values, or power transformations thereof, or cell frequencies yield better results. Note that several criteria, other than the numeric value, may also have an impact on a user’s perception of a particular cells importance, such as its situation within the table (totals and sub-totals are often rated as highly important), or its category (certain categories of variables are often considered to be of secondary importance). \(\tau\)-ARGUS offers special facilities to choose a cost function and to carry out power transformations of the cost function:

Cost function

The cost function indicates the relative importance of a cell. In principle the user could attach a separate cost to each individual cell, but that will become a rather cumbersome operation. Therefore in \(\tau\)‑ARGUS a few standard cost functions are available2:

2 One of the secondary cell suppression methods of \(\tau\)-ARGUS, the hypercube method, uses an elaborate internal weighting scheme in order to avoid to some extent the suppression of totals and subtotals which is essential for the performance of the method. In order to avoid that this internal weighting scheme is thrown out of balance, it has been decided to make the cost function facilities of t-ARGUS inoperational for this method.

- Unity, i.e. all cells have equal weight (just minimising the number of suppressions)

- The number of contributors (minimising the number of contributors to be hidden)

- The cell value itself (preserving as much as possible the largest – usually most important – cells)

- The cell value of another variable in the dataset (this will be the indication of the important cells).

Especially in the latter two cases the cell value could give too much preference to the larger cells. Is a 10 times bigger cell really 10 times as important? Sometimes there is a need to be a bit more moderate. Some transformation of the cost function is desired. Popular transformations are square-root or a log-transformation. Box and Cox (1960) have proposed a system of power transformations:

\[ y = \frac{x^{\lambda} -1}{\lambda} \]

In this formula \(\lambda = 0\) yields to a log-transformation and the \(-1\) is needed for making this formula continuous in \(\lambda\).

This last aspect and the fact that this could lead to negative values we have introduced a simplified version of the lamda-transformation in \(\tau\)‑ARGUS

\[ y = \begin{cases} x^{\lambda} \quad &\text{for }\lambda\neq0 \\ \text{log}(x)\quad &\text{for }\lambda=0 \end{cases} \]

So choosing \(\lambda = \frac{1}{2}\) will give the square-root.

4.3.2 Evaluation of Secondary Cell Suppression algorithms offered by \(\tau\)‑ARGUS

The software package \(\tau\)−ARGUS offers a variety of algorithms to assign secondary suppressions which will be described in detail in Section 4.4. While some of those algorithms are not yet fully developed, or not yet fully integrated into the package, respectively, two are indeed powerful tools for automated tabular data protection. In this section we focus on those latter algorithms. We compare them with respect to quality aspects of the protected tables, while considering also some practical issues. Based on this comparison, we finally give some recommendation on the use of those algorithms.

We begin this section by introduction of certain minimum protection standards PS1, and PS2. We explain why it is a ‘must’ for an algorithm to satisfy those standards in order to be useable in practice. For those algorithms that qualify ‘useable’ according to these criteria, we report some results of studies comparing algorithm performance with regard to information loss, and disclosure risk.

In Section 4.2.2 we have defined criteria for a safe suppression pattern. It is of course possible to design algorithms that will ensure that no suppression pattern is considered feasible unless all of these criteria are satisfied. In practice, however, such an algorithm would either require too much computer resource (in particular: CPU time) when applied to the large, detailed tabulations of official statistics, or the user would have to put up with a strong tendency for oversuppression. In the following, we therefore define minimum standards for a suppression pattern that is safe w.r.t. the safety rule adopted except for a residual disclosure risk that might be acceptable to an agency. It should be noted that those standards are definitely superior, or at least equal to what could be achieved by the traditional manual procedures for cell suppression, even if carried out with utmost care! For the evaluation, we consider only those algorithms that ensure validity of the suppression pattern at least with respect to those relaxed standards.

Minimum protection standards

For a table with hierarchical substructure, feasibility intervals computed on basis of the set of equations for the full table normally tend to be much closer than those computed on basis of separate sets of equations corresponding to sub-tables without any substructure. Moreover, making use of the additional knowledge of a respondent, who is the single respondent to a cell (a so called ‘singleton’), it is possible to derive intervals that are much closer than without this knowledge3.

3 Consider for instance the table of example 3 in Section 4.2.2. Without additional knowledge the bounds for cell (1,1) are \(X_{11}^\text{min} = 3\) and \(X_{11}\text{max} = 6\). However, if cell (1,2) were a singleton-cell (a cell with only a single contributor) then this single contributor could of course exactly compute the cell value of cell (1,1) by subtracting her own contribution from the row total of row 1.

Based on the assumption of a simple but probably more realistic disclosure scenario where intruders will deduce feasibility intervals separately for each sub-table, rather than taking the effort to consider the full table, and that single respondents, using their special additional knowledge, are more likely attempting to reveal other suppressed cell values when they are within the same row or column (more general: relation), the following minimum protection standards (PS) make sense:

(PS1) Protection against exact external disclosure:

With a valid suppression pattern, it is not possible to disclose the value of a sensitive cell exactly, if no additional knowledge (like that of a singleton) is considered, and if subsets of table equations are considered separately, i.e. when feasibility intervals are computed separately for each sub-table.(PS2) Protection against singleton disclosure:

A suppression pattern, with only two suppressed cells within a row (or column) of a table is not valid, if each of the two corresponds to a single respondent who are not identical.(PS1*) extension of (PS1) for inferential (instead of exact) disclosure,

(PS2*) extension of (PS2), covering the more general case where a single respondent can disclose another single respondent cell, not necessarily located within the same row (or column) of the table.

\(\tau\)-ARGUS offers basically two algorithms, Modular and Hypercube, both satisfying the above-mentioned minimum standards regarding disclosure risk. Both take a backtracking approach to protect hierarchical tables within an iterative procedure: they subdivide hierarchical tables into sets of linked, unstructured tables. The cell suppression problem is solved for each subtable separately. Secondary suppressions are coordinated for overlapping subtables.

The Modular approach, a.k.a. HiTaS algorithm (see de Wolf, 2002), is based on the optimal solution as implemented by Fischetti and Salazar-González. By breaking down the hierarchical table in smaller non-structured subtables, protecting these subtables and linking the subtables together by a backtracking procedure the whole table is protected. For a description of the modular approach see Section 4.4.2, the optimal Fischetti/Salazar-González method is described in section Section 4.4.1. See also Fischetti and Salazar-González (2000).

The Hypercube is based on a hypercube heuristic implemented by Repsilber (2002). See also the descriptions of this method in Section 4.4.4.

Note that in the current implementation of \(\tau\)-ARGUS, use of the optimization tools requires a license for additional commercial software (LP-solver), whereas use of the hypercube method is free. While Modular is only available for the Windows platform, of Hypercube there are also versions for Unix, IBM (OS 390) and SNI (BS2000).

Both Modular and Hypercube provide sufficient protection according to standards PS1* (protection against inferential disclosure) and PS2 above. Regarding singleton disclosure, Hypercube even satisfies the extended standard PS2*. However, simplifications of the heuristic approach of Hypercube cause a certain tendency for oversuppression. This evaluation therefore includes a relaxed variant that, instead of PS1*, satisfies only the reduced standard PS1, i.e. zero protection against inferential disclosure. We therefore refer to this method as Hyper0 in the following. Hyper0 processing can be achieved simply by deactivating the option “Protection against inferential disclosure required” when running Hypercube out of \(\tau\)‑ARGUS.

| Algorithm | Modular | Hypercube | Hyper0 | |

| Procedure for secondary suppression | Fischetti/Salazar optimization | Hypercube heuristic | ||

| Protection standard | Interval/Exact disclosure | PS1* | PS1* | PS1 |

| Singleton | PS2 | PS2* | PS2* | |

In the following, we briefly report results of two evaluations studies, in the following referred to as study A, and study B. For further detail on these studies see Giessing (2004) for study A, and Giessing et al. (2006) for study B. Both studies are based on tabulations of a strongly skewed magnitude variable.

For study A, we used a variety of hierarchical tables generated from the synthetic micro‑data set supplied as CASC deliverable 3-D3. In particular, we generated 2- and 3-dimensional tables, where one of the dimensions had a hierarchical structure. Manipulation of the depth of this hierarchy resulted in 7 different tables, with a total number of cells varying between 460 and 150,000 cells. Note that the Hyper0 method was not included in study A.

For study B, which was carried out on behalf of the German federal and state statistical offices, we used 2-dimensional tables of the German turnover tax statistics. Results have been derived for tables with 7-level hierarchical structure (given by the NACE economy classification) of the first dimension, and 4‑level structure of the second dimension given by the variable Region.

We compare the loss of information due to secondary suppression in terms of the number and cell values of secondary suppression, and analyze the disclosure risk of the protected tables. Table 4.6 reports the results regarding the loss of information obtained in study A.

| Table Hier. levels | No. Cells | No. Suppressions (%) | Added Value of Suppressions (%) | |||

|---|---|---|---|---|---|---|

| Hypercube | Modular | Hypercube | Modular | |||

| 2-dimensional tables | ||||||

| 1 | 3 | 460 | 6.96 | 4.35 | 0.18 | 0.05 |

| 2 | 4 | 1,050 | 10.95 | 8.29 | 0.98 | 0.62 |

| 3 | 6 | 8,230 | 14.92 | 11.48 | 6.78 | 1.51 |

| 4 | 7 | 16,530 | 14.97 | 11.13 | 8.24 | 2.12 |

| 3-dimensional tables | ||||||

| 5 | 3 | 8,280 | 14.63 | 10.72 | 6.92 | 1.41 |

| 6 | 4 | 18,900 | 17.31 | 15.41 | 12.57 | 3.55 |

| 7 | 6 | 148,140 | 15.99 | 10.63 | 23.16 | 3.91 |

Table 4.7 presents information loss results from study B on the two topmost levels of the second dimension variable Region, e.g. on the national, and state level.

| Algorithm for secondary suppression | Number | Added Value | |||

|---|---|---|---|---|---|

| State level | National level | overall | |||

| abs | % | abs | % | % | |

| Modular | 1,675 | 10.0 | 7 | 0.6 | 2.73 |

| Hyper0 | 2,369 | 14.1 | 8 | 0.7 | 2.40 |

| Hypercube | 2,930 | 17.4 | 22 | 1.9 | 5.69 |

Both studies show that best results are achieved by the modular method, while using either variant of the hypercube method leads to an often quite considerable increase in the amount of secondary suppression compared to the result of the modular method. The size of this increase varies between hierarchical levels of the aggregation: on the higher levels of a table the increase tends to be even larger than on the lower levels. Considering the results of study B presented in Table 4.7, on the national level we observe an increase of about 214% for Hypercube (14% for Hyper0), compared to an increase of 75% (41%) on the state level. In Giessing et al. (2006) we report also results on the district level. On that level the increase was about 28% on the higher NACE levels for Hypercube (9% for Hyper0), and 20 % for Hypercube (14% for Hyper0) on the lower levels. In study A we observed increases mostly around 30% for Hypercube, for the smallest 2‑dimensional, and the largest 3-dimensional instance even of 50% and 60%, respectively. In particular, our impression is that the hypercube method tends to behave especially badly (compared to Modular), when tabulations involve many short equations, with only a few positions.

A first conclusion from the results of study B reported above was, because of the massive oversuppression, to exclude the Hypercube method in the variant that prevents inferential disclosure from any further experimentation. Although clearly only second-best performer, testing with Hyper0 was to be continued, because of technical and cost advantages mentioned above.

In experiments with state tables where the variable Region was taken down to the community level, we found that this additional detail in the table caused an increase in suppression at the district level of about 70 – 80% with Hyper0 and about 10 – 30% with Modular.

Disclosure risk

As explained in Section 4.2.2, in principle, there is a risk of inferential disclosure, when the bounds of the feasibility interval of a sensitive cell could be used to deduce bounds on an individual respondent’s contribution that are too close according to the method employed for primary disclosure risk assessment. However, for large, complex structured tables, this risk is rather a risk potential, not comparable to the disclosure risk that would result from a publication of that cell. After all, the effort connected to the computation of feasibility intervals based on the full set of table equations is quite considerable. Moreover, in a part of the disclosure risk cases only insiders (other respondents) would actually be able to disclose the individual contribution.

Anyway, with this definition, and considering the full set of table equations, in study B we found between about 4% (protection by Modular) and about 6% (protection by Hyper0) of sensitive cells at risk in an audit step where we computed the feasibility intervals for a tabulation by NACE and state, and for two more detailed tables (down to the district level) audited separately for two of the states. In study A, we found up to about 5.5% (1.3%) cells at risk for the 2-dimensional tables protected by Modular (Hypercube, resp.), and for the 3-dimensional tables up to 2.6% (Modular) and 5.6% (Hypercube).

Of course, the risk potential is much higher for at-risk cells when the audit is carried out separately for each subtable without substructure, because the effort for this kind of analysis is much lower. Because Modular protects according to PS1* standard, there are no such cells in tables protected by Modular. For Hyper0, in study B we found about 0.4% cells at risk, when computing feasibility intervals for several subtables of a detailed tabulation.

For those subtables, when protected by Modular, for about 0.08% of the singletons, it turned out that another singleton would be able to disclose its contribution. Hyper0 satisfies PS2* standard, therefore of course no such case was found, when the table was protected by Hyper0.

Recommendation

The methods Modular and Hypercube of \(\tau\)‑ARGUS are powerful tools for secondary cell suppression. Concerning protection against external disclosure both satisfy the same protection standard. However, Modular gives much better results regarding information loss. Even compared to a variant of Hypercube (Hyper0) with relaxed protection standard, Modular performs clearly better. Although longer computation times for this method (compared to the fast hypercube method) can be a nuisance in practice, the results clearly justify this additional effort – after all, it is possible, for instance, to protect a table with detailed hierarchical structure in two dimensions and more than 800,000 cells within just about an hour. Considering the total costs involved in processing a survey, it would neither be justified to use Hypercube (or Hyper0) only in order to avoid the costs for the commercial license which is necessary to run the optimization tools of Modular.

We also recommend use of Modular to assign secondary suppressions in 3-dimensional tables. However, when those tables are given by huge classifications, long computation times may become an actual obstacle. It took us, for instance, about 11 hours to run a 823 x 18 x 10 table (first dimension hierarchical). The same table was protected by Hyper0 within about 2 minutes. Unfortunately, replacing Modular by Hyper0 in that instance leads to about 28% increase in the number of secondary suppressions.

According to our findings, we would expect the Hypercube method (i.e. Hyper0) to be good alternative to Modular, if

- Tabulations involve more than 2 dimensions and are very large, and

- the majority of table equations (e.g. rows, columns, …) are long, involving many positions, and